Introduction

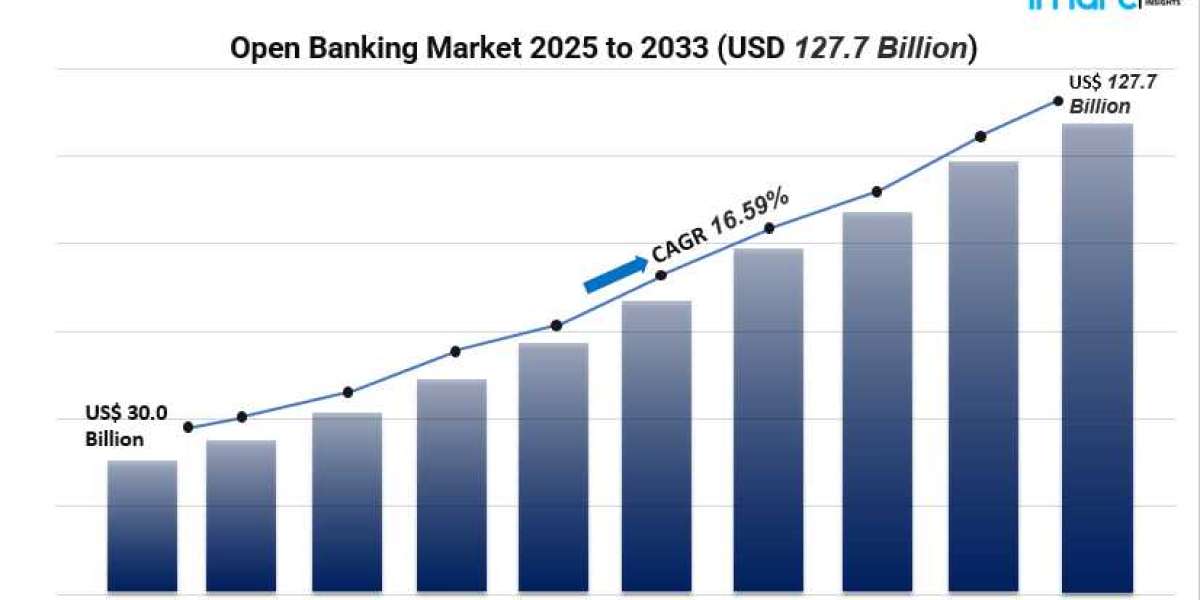

The global open banking market surged to USD 30 billion in 2024 and is projected to reach around USD 127.7 billion by 2033, growing at a 16.59% CAGR. This dynamic expansion is fueled by robust fintech investments, tech-driven API advancements, supportive regulations, and soaring demand for personalized, transparent digital banking experiences .

Study Assumption Years

- Base Year: 2024

- Historical Year: 2019–2024

- Forecast Year: 2025–2033

Open Banking Market Key Takeaways

- Europe leads the market due to mandates like PSD2, driving strongest regional growth.

- Banking capital markets is the dominant service, followed by payments, digital currencies, and value-added services.

- On-premises deployment tops preference for data control and compliance, while cloud-based adoption grows.

- App markets lead as distribution channels, supported by rising consumer adoption of mobile banking.

- Market size is USD 30 billion in 2024, previsaged to rise to USD 127.7 billion by 2033 at a CAGR of 16.59%.

Market Growth Factors

- Technological advancement in APIs AI

Open banking is really taking off, and a big part of that is thanks to the rise of advanced API integration and AI-driven personalization. Secure APIs are essential for enabling smooth access for third parties, which fosters collaboration between banks and fintech companies. Just take a look at Europe—by 2022, there were over 9,000 fintech startups! It’s evident that API innovation is reshaping the digital finance landscape. With the help of AI and machine learning, we can now provide real-time personalized advice, which really boosts customer engagement, satisfaction, and loyalty. As financial institutions aim for cutting-edge infrastructure, API ecosystems are evolving to improve fraud prevention, data validation, and scalable analytics. Meanwhile, AI-powered platforms are digging into consumer behavior, offering investment insights, tailored credit scoring, and predictive budgeting tools. This dynamic duo of APIs and AI not only broadens the market but also speeds up the adoption of open banking ecosystems across various sectors. - Regulatory frameworks boosting openness

Supportive regulations—like PSD2 in Europe and the UK's Open Banking rules—are crucial for the sector's growth by mandating data-sharing APIs. The requirement for account access under PSD2 has ignited competition and innovation, resulting in nearly 2,500 registered third-party providers in Europe. These regulations have also played a significant role in building consumer trust through strict GDPR measures. In the UK, the CMA's requirements for major banks have driven API calls to over one billion in 2023. Consistent regulations and cross-border compliance have created a robust environment for secure data exchange, allowing both established banks and agile fintechs to enhance their open banking capabilities. This well-structured environment eases security concerns, aligns standards, and ensures widespread market adoption. - Rising consumer demand for personalized banking

Consumers are increasingly seeking financial services that cater to their individual needs in real-time. In fact, over 60% of users in Europe are actively searching for personalized banking experiences that utilize data-driven insights. Open banking is stepping up to fulfill this demand by enabling third-party innovations like budgeting tools, tailored lending options, and investment platforms. By the end of 2021, the UK saw daily open banking log-ins soar to around 2 million. These impressive engagement figures are encouraging banks to collaborate with fintech companies to develop richer, more personalized solutions for their customers. Additionally, as consumer education and trust in security improve through regulated transparency, adoption rates are on the rise. With digital-native generations leaning towards seamless, personalized financial services, open banking’s ability to combine convenience with customization is driving market growth and deeper integration in both retail and commercial banking.

Request for a sample copy of this report: https://www.imarcgroup.com/open-banking-market/requestsample

Market Segmentation

Breakup by Services

- Banking and Capital Markets: Dominates due to customer preference, tech development regulation.

- Payments: Covers innovations in money transfer and digital payment services.

- Digital Currencies: Includes blockchain-based payments and crypto integrations.

- Value Added Services: Encompasses budgeting tools, analytics, and other enhancements.

Breakup by Deployment

- Cloud-based: Remote, scalable API hosting in cloud environments.

- On‑premises: In‑house solutions preferred for security, compliance, control.

Breakup by Distribution Channel

- Bank Channels: Traditional bank platforms enabling open banking.

- App Markets: Mobile apps offering fintech services—leading channel.

- Distributors: Intermediaries distributing open banking solutions.

- Aggregators: Platforms bundling multi‑bank data streams.

Breakup by Region

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Regional Insights

Europe is leading the way in the open banking landscape, thanks to PSD2 mandates and GDPR-backed data regulations that promote transparent API access. With over 2,500 registered third-party providers, Europe is at the forefront of fintech collaboration, regulatory clarity, and consumer trust—propelling market value and innovation across the region.

Recent Developments News

In July 2023, Fintonic launched OpenInsights, a data analytics platform that transforms open banking data into actionable insights for businesses, enhancing strategic understanding and consumer awareness. In October 2022, GoCardless teamed up with Crowdz to enable faster, cross-border SME payments through open banking integration—featuring verified mandates and middleware to securely streamline transactions across the UK, US, and EU. These advancements underscore the shift towards analytics-driven services and seamless international funding solutions.

Key Players

- Banco Bilbao Vizcaya Argentaria S.A.

- Clarity Group Inc.

- Credit Agricole (SAS Rue La Boétie)

- Finastra (Misys International Limited)

- Finleap connect

- Jack Henry Associates Inc

- Mambu

- NCR Corporation

- Nordigen Solution

- Revolut Ltd

- Riskonnect Inc.

- Societe Generale

Ask Analyst for Customization: https://www.imarcgroup.com/request?type=reportid=6327flag=C

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include a thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape, and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: +1-631-791-1145