IMARC Group, a leading market research company, has recently released a report titled "String Inverter Market Report by Connection Type (On-Grid, Off-Grid), Phase (Single Phase, Three Phase), Power Rating (Up to 10kW, 11kW to 40kW, 41kW to 80kW, Above 80kW), End Use (Residential, Commercial and Industrial, Utilities), and Region 2025-2033." The study provides a detailed analysis of the industry, including the global string inverter market size, share, trends, and growth forecast. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

String Inverter Market Highlights:

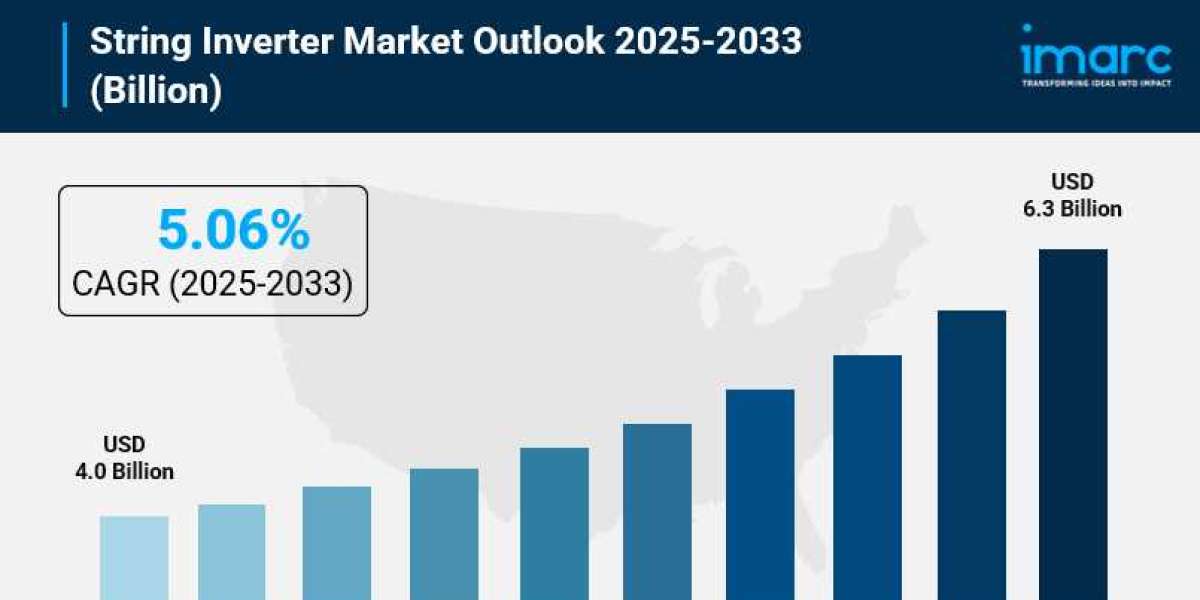

- String Inverter Market Size: Valued at USD 4.0 Billion in 2024.

- String Inverter Market Forecast: The market is expected to reach USD 6.3 billion by 2033, growing at an impressive rate of 5.06% annually.

- Market Growth: The string inverter market is experiencing steady growth driven by expanding solar energy adoption and supportive government renewable energy policies worldwide.

- Technology Integration: Advanced technologies like smart grid connectivity, remote monitoring capabilities, and enhanced efficiency features are transforming string inverter performance and reliability.

- Regional Leadership: Asia-Pacific leads the global market, driven by massive solar installations in China and India, along with aggressive renewable energy targets across the region.

- Cost Competitiveness: Declining solar photovoltaic component prices and improved manufacturing efficiencies are making string inverters more accessible to residential, commercial, and utility-scale projects.

- Key Players: Industry leaders include Huawei Technologies, Sungrow Power Supply, SMA Solar Technology, SolarEdge Technologies, and other major manufacturers dominating the market with innovative solutions.

- Market Challenges: Grid integration issues, curtailment in high-penetration areas, and balancing supply-demand dynamics present ongoing challenges for market participants.

Claim Your Free “String Inverter Market” Insights Sample PDF: https://www.imarcgroup.com/string-inverter-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Industry Trends and Drivers:

- Explosive Growth in Solar Energy Adoption:

The global solar energy sector is witnessing unprecedented expansion, creating massive demand for efficient power conversion equipment. China installed 277 GW of solar capacity in 2024 alone, representing 45.2% year-over-year growth and bringing its cumulative installed solar power capacity to 890 GW. India has emerged as the world's third-largest solar market, adding a record 24 GW of solar capacity in 2024—more than double the installations from the previous year. This remarkable surge in solar photovoltaic deployments is creating enormous pressure on manufacturers to deliver high-performance string inverters that can handle increasing power loads while maintaining reliability and efficiency across diverse installation environments.

- Aggressive Government Support and Policy Frameworks:

Governments worldwide are implementing robust policy frameworks to accelerate the transition to renewable energy. The European Union has set a target to achieve 32% of its energy from renewable sources by 2030, driving substantial investments in solar infrastructure across member states. India reached a significant milestone by achieving 50% of its installed electricity capacity from non-fossil fuel sources in July 2025—five years ahead of its Paris Agreement commitments—with total renewable energy capacity reaching 234 GW. The United States maintained its Investment Tax Credit providing 30% cost reduction for solar installations through the end of 2025, though policy changes are creating urgency among residential and commercial buyers to complete projects before incentive modifications take effect.

- Dramatic Cost Reductions Making Solar Economically Compelling:

The economics of solar energy have fundamentally transformed over the past decade, with the weighted average cost of electricity from utility-scale solar PV falling by 85% between 2010 and 2020 according to IRENA data. This dramatic price compression has made solar power one of the cheapest forms of electricity generation in most countries, often significantly more affordable than fossil fuel alternatives. In the Asia-Pacific region specifically, industry reports indicate that utility-based solar photovoltaic prices have made renewable energy 13% more cost-effective than coal as of 2024. China leads globally in cost reduction, with offshore wind, utility PV, and onshore wind being 40% to 70% more affordable than in other Asian markets. These favorable economics are driving unprecedented adoption rates across both developed and emerging markets.

- Technological Innovation Enhancing Performance and Reliability:

String inverter manufacturers are rapidly advancing their technological capabilities to meet evolving market demands. In September 2024, Solis launched two new string inverters—the S5-GC125K-US (125 kW) and S5-GC60K-LV-US (60 kW)—for the US and Canadian markets, offering maximum efficiency of 98.5% with multiple MPPT channels and fuse-free architecture. In 2023, Kaco New Energy introduced the NX1 M2 product range with four versions offering outputs from 3.0 to 5.0 kVA, achieving 97.5% maximum efficiency and 96.9% European efficiency ratings. Pyramid Electronics unveiled three-phase string inverters incorporating silicon carbide (SiC) technology to deliver higher power conversion efficiencies and greater power density, available in 5 kW to 15 kW ratings with 1,000 V input DC voltage. These innovations demonstrate the industry's commitment to pushing efficiency boundaries while reducing system costs and improving operational reliability.

String Inverter Market Report Segmentation:

Breakup by Connection Type:

- On-Grid

- Off-Grid

On-grid systems dominate the market, benefiting from integration with existing power infrastructure, net metering opportunities, and financial incentives that make grid-connected installations particularly attractive for urban and suburban applications.

Breakup by Phase:

- Single Phase

- Three Phase

Three-phase inverters command the largest market share due to their high efficiency and suitability for large-scale commercial, industrial, and utility solar installations requiring substantial energy output and balanced power supply capabilities.

Breakup by Power Rating:

- Up to 10kW

- 11kW to 40kW

- 41kW to 80kW

- Above 80kW

The 41kW to 80kW segment represents the leading market segment, offering an optimal balance of capacity, compact design, and flexibility for medium to large-scale photovoltaic installations across various application types.

Breakup by End Use:

- Residential

- Commercial Industrial

- Utilities

Utilities represent a significant market segment, driven by large-scale solar power plants and solar parks where string inverters provide cost-effective power conversion for multi-megawatt installations serving grid-connected applications.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia-Pacific dominates the global string inverter market, driven by China's massive solar capacity additions, India's aggressive renewable energy targets, and expanding solar installations across Southeast Asian nations seeking energy security and sustainability.

Who are the key players operating in the industry?

The report covers the major market players including:

- Huawei Technologies Co., Ltd.

- Sungrow Power Supply Co., Ltd.

- SMA Solar Technology AG

- SolarEdge Technologies Inc.

- TBEA Xinjiang SunOasis Co., Ltd.

- Delta Energy Systems Inc.

- KSTAR New Energy Co. Ltd.

- Sineng Electric Co. Ltd.

- Enphase Energy Inc.

- ABB Ltd.

- Fronius International GmbH

- Ginlong Technologies Co., Ltd.

- GoodWe Technologies Co., Ltd.

Ask Analyst For Request Customization: https://www.imarcgroup.com/request?type=reportid=4638flag=E

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services.

IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1–201971–6302