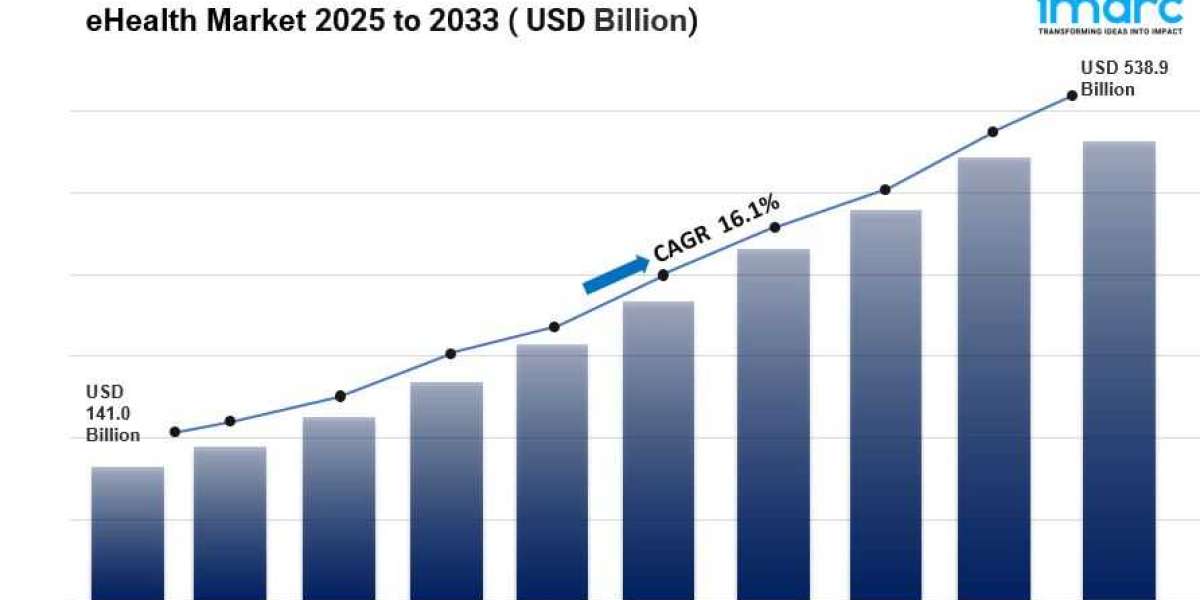

The global eHealth market Trends was valued at USD 141.0 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 538.9 Billion by 2033, exhibiting a CAGR of 16.1% during 2025-2033. North America currently dominates the market, holding a significant market share of over 38.7% in 2024. The market is experiencing steady growth driven by technological advancements, the increasing prevalence of chronic diseases, government initiatives promoting digital health, the growing demand for remote patient monitoring and telehealth services, and enhanced patient engagement through mobile health applications.

Key Stats for eHealth Market:

- eHealth Market Value (2024): USD 141.0 Billion

- eHealth Market Value (2033): USD 538.9 Billion

- eHealth Market Forecast CAGR: 16.1%

- Leading Product Segment in eHealth Market in 2024: mHealth (27.9%)

- Leading Service Segment: Monitoring Services (62.0%)

- Leading End User Segment: Healthcare Providers (51.7%)

- Key Regions in eHealth Market: North America, Europe, Asia Pacific, Latin America, Middle East and Africa

- Top companies in eHealth Market: Allscripts Healthcare Solutions Inc., Athenahealth, Cerner Corporation, Doximity Inc., Epic Systems Corporation, General Electric Company, International Business Machines Corporation, Koninklijke Philips NV, Medisafe Limited (Steris plc), SetPoint Medical Corporation, Telecare Corporation, etc.

Why is the eHealth Market Growing?

The eHealth market is experiencing explosive growth as healthcare systems worldwide embrace digital transformation. What started as a gradual shift has accelerated into a full-scale revolution, fundamentally changing how medical care is delivered, monitored, and managed.

The pandemic served as a massive catalyst. According to the Centers for Disease Control and Prevention, nearly 95% of health centers reported using telehealth services during the pandemic—a dramatic jump from just 43% previously. What's remarkable is that this trend hasn't reversed. McKinsey Company reports that overall telehealth utilization for office visits and outpatient care is now 78 times greater than it was in early 2020. This isn't temporary—it's the new normal.

Electronic health records represent another transformation story. About 96% of non-federal acute care hospitals and 78% of office-based physicians now use certified EHR systems, according to HealthIT. That's a complete reversal from a decade ago when only 28% of hospitals and 34% of physicians had such systems. This widespread adoption is improving patient care dramatically by facilitating better information sharing, reducing medical errors, and enhancing overall healthcare coordination.

Mobile health applications are surging in popularity, driven by smartphone penetration and consumers' appetite for health self-management. The mHealth segment captures 27.9% of the market, reflecting how people want healthcare at their fingertips. These apps enable patients to monitor their health, manage chronic conditions like diabetes and hypertension, and communicate with healthcare providers—all from their phones.

Europe is making impressive strides toward digital health accessibility. The EU's composite eHealth score reached 83%, representing a 4-percentage-point increase from the previous year. All member states now provide some form of online access for citizens to view their health data, with twenty-three countries offering centralized electronic health record access. The EU is on track toward its ambitious target of 100% citizen access to electronic health records by 2030.

The United States dominates North America's eHealth market with 89.70% market share, driven by advanced infrastructure and substantial health IT investments. The HITECH Act has provided crucial government support, offering incentives for eHealth adoption while promoting interoperability. Remote monitoring tools are particularly valuable in areas facing extreme weather events or geographical challenges, enabling timely medical intervention regardless of location.

Asia-Pacific presents enormous growth potential, particularly for populations facing infrastructure challenges. In India, 65% of e-commerce users express acceptance of digital health solutions, according to Arthur D. Little research. This digital familiarity is translating directly into healthcare adoption, with telemedicine bridging gaps in regions lacking adequate medical infrastructure.

Request Customization: https://www.imarcgroup.com/request?type=reportid=3918flag=E

AI Impact on the eHealth Market:

Artificial intelligence is revolutionizing eHealth by enabling predictive diagnostics, personalized treatment plans, and enhanced decision-making. AI algorithms analyze vast datasets from electronic health records, identifying patterns that help clinicians detect diseases earlier and more accurately. Virtual health assistants powered by AI provide 24/7 patient support, answering questions and offering guidance between appointments.

Machine learning enhances remote monitoring by intelligently analyzing data from wearable devices, alerting healthcare providers only when intervention is needed rather than overwhelming them with continuous data streams. Natural language processing improves documentation efficiency, automatically extracting relevant information from clinical notes and reducing administrative burden on physicians.

AI-driven diagnostic tools are demonstrating remarkable accuracy in specialties like radiology and pathology, often matching or exceeding human performance in detecting conditions from medical images. Predictive analytics help hospitals optimize resource allocation, forecasting patient admissions and staffing needs more accurately.

Blockchain integration is emerging as a solution for secure, interoperable health data sharing, addressing privacy concerns while enabling seamless information exchange between healthcare systems. These technologies combined are creating more efficient, accessible, and personalized healthcare experiences for patients worldwide.

Ehealth Market Report Segmentation:

By Product:

- Electronic Health Records

- ePrescribing

- Clinical Decision Support

- Telemedicine

- Consumer Health Information

- mHealth

- Others

mHealth represented the largest segment by product due to the widespread adoption of mobile devices and the convenience they offer for accessing healthcare services remotely.

By Services:

- Monitoring

- Diagnostic

- Healthcare Strengthening

- Others

Monitoring represented the largest segment by services because of the increasing demand for remote patient monitoring solutions, driven by the need for continuous care management and proactive health monitoring.

By End User:

- Healthcare Providers

- Payers

- Healthcare Consumers

- Others

Healthcare providers represented the largest segment by end user as they are the primary users of eHealth solutions for delivering patient care, managing health records, and optimizing clinical workflows.

Regional Insights:

- North America

- Asia-Pacific

- Europe

- Latin America

- Middle East and Africa

North America was the largest market for eHealth solutions regionally, attributed to factors such as technological advancements, supportive government policies, and high healthcare spending in the region.

Speak to An Analyst: https://www.imarcgroup.com/request?type=reportid=3918flag=C

Key Companies:

- Allscripts Healthcare Solutions Inc.

- Athenahealth Inc.

- Cerner Corporation

- Doximity Inc.

- Epic Systems Corporation

- General Electric Company

- International Business Machines Corporation

- Koninklijke Philips NV

- Medisafe Limited (Steris plc)

- SetPoint Medical Corporation

- Telecare Corporation

If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services.

IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201971-6302