Market Overview 2025-2033

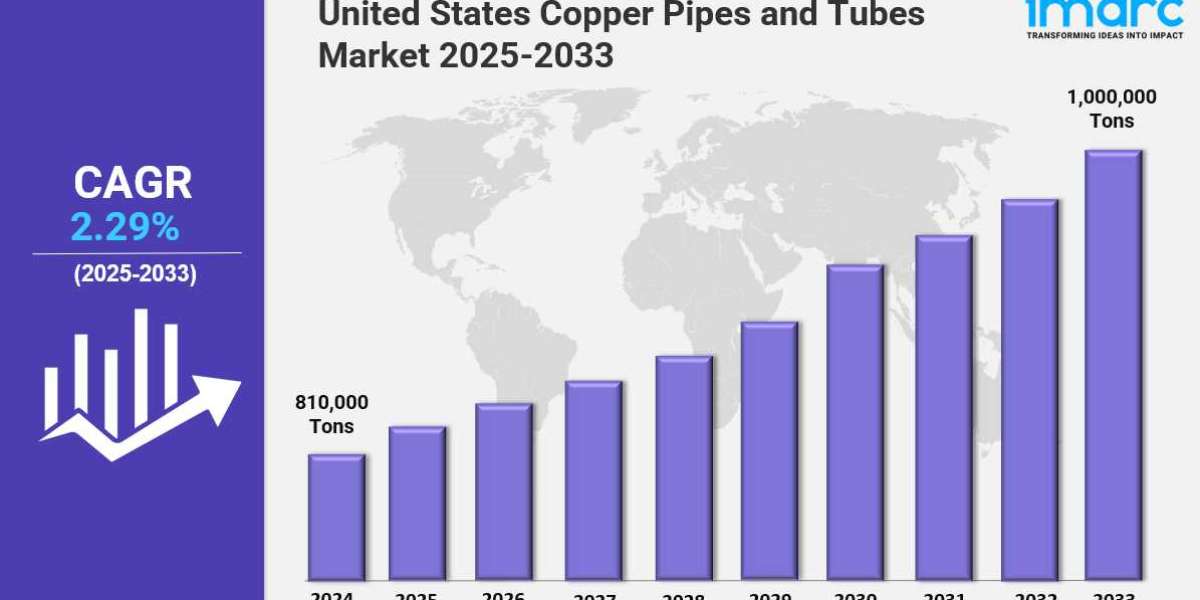

The United States copper pipes and tubes market size reached 810,000 Tons in 2024. Looking forward, IMARC Group expects the market to reach 1,000,000 Tons by 2033, exhibiting a growth rate (CAGR) of 2.29% during 2025-2033. The industry is witnessing steady growth driven by rising demand in construction, plumbing, and HVAC systems. Technological advancements, infrastructure upgrades, and sustainability trends are boosting adoption. Increased urbanization and renovation activities further contribute to the expanding market landscape across the country.

Key Market Highlights:

✔️ Strong market growth driven by increasing demand in HVAC, plumbing, and industrial applications

✔️ Rising preference for durable, corrosion-resistant, and energy-efficient copper solutions

✔️ Expanding investments in construction, infrastructure, and renewable energy sectors

Request for a sample copy of the report: https://www.imarcgroup.com/united-states-copper-pipes-tubes-market/requestsample

United States Copper Pipes and Tubes Market Trends and Drivers:

The United States copper pipes and tubes market continues to grow steadily, supported by major infrastructure investments and sustained construction activity in both residential and commercial sectors. Federal programs like the Infrastructure Investment and Jobs Act have directed substantial funding toward updating water systems, HVAC installations, and industrial plants—core applications where copper remains the preferred material due to its strength, thermal conductivity, and corrosion resistance.

As of 2024, non-residential construction—including data centers, semiconductor manufacturing sites, and renewable energy installations—accounted for over 35% of total copper pipe usage across the country. The market continues to benefit from national building codes that prioritize safety and performance, giving copper an edge over alternatives like PVC and PEX. These standards are reinforcing United States copper pipes and tubes market demand, particularly in sectors requiring fire-resistant and long-lasting materials.

However, rising raw material costs and increased competition from composite and polymer-based systems have begun to pressure margins. In response, U.S. manufacturers are investing in advanced copper alloys that offer greater efficiency at reduced weight and cost. Copper’s recyclability is also becoming more important. By 2024, recycled copper accounted for nearly 45% of total domestic use, boosted by incentives in green building programs and corporate sustainability targets. These trends have become central to United States copper pipes and tubes market growth, as improved recycling practices lower manufacturing costs and help stabilize supply chains.

Supply chain risks remain a concern. The U.S. continues to import around 60% of its refined copper, primarily from Chile, Peru, and Canada. To encourage local production, new tariffs on imported copper tubes were enacted in 2024. Domestic output increased by 12% year-over-year, though copper prices also rose by 18% during the same period, reflecting global supply constraints and ongoing price volatility.

Other sectors such as automotive, HVAC manufacturing, and electronics—traditionally heavy users of precision copper tubing—are beginning to evaluate aluminum and composite substitutes due to rising costs. In response, American producers are expanding local smelting operations and investing in digital logistics platforms to reduce reliance on imported materials and improve supply chain resilience.

In terms of volume, the United States copper pipes and tubes market size reached 810,000 tons in 2024. This milestone reflects a broader trend toward modernization in the industry. Over a quarter of domestic producers have now adopted smart manufacturing practices, including IoT-based quality monitoring and predictive maintenance systems. These upgrades have reduced production downtime by up to 30%, increasing efficiency and output.

Healthcare infrastructure is also contributing to demand. In response to updated hygiene regulations, 15 states now require antimicrobial copper piping in hospitals and medical facilities. At the same time, copper's role in the clean energy sector is expanding. With more electric vehicle (EV) charging stations and solar thermal systems being built nationwide, demand for durable and conductive tubing continues to grow beyond traditional construction.

Challenges such as inflation, energy costs, and regulatory uncertainty continue to affect the sector. To offset these pressures, manufacturers and distributors are focusing on vertical integration and forming long-term supply agreements to secure raw materials and maintain stable pricing.

Looking ahead, the United States copper pipes and tubes market outlook remains positive. With continued investment in smart cities, clean energy infrastructure, and water system upgrades, the industry is positioned for stable, long-term growth. Market volume is expected to rise from 810,000 tons in 2024 to approximately 1,000,000 tons by 2033, with a projected CAGR of 2.29%. As the country prioritizes sustainability and resilience in construction and energy, copper will remain a key material in national development plans.

United States Copper Pipes and Tubes Market Segmentation:

The report segments the market based on product type, distribution channel, and region:

Study Period:

Base Year: 2024

Historical Year: 2019-2024

Forecast Year: 2025-2033

Breakup by Finish Type:

- LWC Grooved

- Straight Length

- Pan Cake

- LWC Plain

Breakup by Outer Diameter:

- 3/8, 1/2, 5/8 Inch

- 3/4, 7/8, 1 Inch

- Above 1 Inch

Breakup by End User:

- HVAC

- Industrial Heat Exchanger

- Plumbing

- Electrical

- Others

Breakup by Region:

- Northeast

- Midwest

- South

- West

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145